| Monthly India Treasury Update |

| Monday, 1 April 2013 |

| |

| Defeat ― I do not recognise the meaning of the word! ~ Margaret Thatcher |

| |

| This report must be read with the disclosures at the conclusion of the report. |

| |

| Domestic Markets |

| |

| Rupee ended marginally higher on continued dollar selling by foreign institutional investors and year end dollar supply |

|

|

|

March Closing Rate – 54.31/54.32 (previous month close – 54.37/54.38) |

|

|

|

After touching a high of 55.1500 at the start of the month, rupee strengthened against USD in the first half of March and remained range bound thereafter. Year end dollar supply from exporters hit the market, directing the spot move lower which was further supported by continued investment by FIIs in the Indian equities. Better than expected trade data also supported the move |

|

| |

| Indian Equity Markets ended flat amidst political uncertainties and local fund redemption pressure |

|

|

|

BSE index March closing– 18,835.77 (down 0.13% from Feb close) |

|

|

|

Indian Equity Markets closed almost flat over the last month’s closing, as the local redemption pressure led to domestic mutual funds divesting equities and political uncertainties over the survival of the central government gave jitters to the investors. The FII buying interest continued, supporting the local equities. The central bank delivered a rate cut of 0.25% providing further support to the equities |

|

|

|

FII Equity flows March: Net USD +1912.52 MIO investment |

|

| |

| Indian Bonds Market ended lower on political uncertainties and reduced expectations of future easing by the central bank |

|

|

|

8.15 percent Government bond 2022 yield – 7.9500 percent (Up 8 bps over previous month close of 7.9100 percent) |

|

|

|

Indian Bonds broke the streak of three month rally to end the month lower, as political uncertainties over survival of central government, after a key ally took away their support, spooked the investors. The RBI also gave a very cautious commentary in their monetary policy announcement, reducing future expectations of easing. However, a 25 bps point cut in the key policy rate kept the bond prices supported |

|

|

|

FII Debt flows March: Net USD +923.92 MIO investment |

|

| |

| Key Local Policy Initiatives and Government Actions |

|

|

|

RBI delivered a 25 bps rate cut in the key policy rate |

|

|

|

Finance ministry announced rationalisation of the FII debt limits wherein: |

|

|

|

| 1. |

The existing debt limit are merged in the two broad categories; Government securities of US$ 25 billion and Corporate bonds of US$ 51 billion |

|

|

| 2. |

The entire limit in both the Government securities and Corporate bonds categories will be made available to all eligible classes of foreign investors, including FIIs, QFIs, and long-term investors such as Sovereign Wealth Funds (SWFs), Pension Funds, Foreign Central Banks, etc. |

|

|

| 3. |

Out of USD 25 billion limit for Government Securities, a sub limit of US$ 5.5 billion has been provided for investment in short-term papers such as treasury bills. Similarly, in case of USD 51 billion limit for corporate bonds, a sub limit of US$ 3.5 billion has been provided for investment in short-term papers such as commercial papers |

|

|

|

|

| |

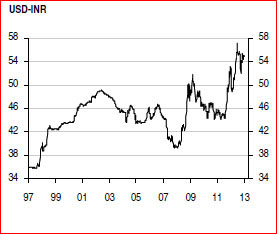

| Snapshot from HSBC Currency Outlook |

|

|

| Source: HSBC March 2013 Currency Outlook |

|

| India - Temporary disappointment? |

|

|

Contrary to market expectations, the Indian government's Union Budget was not able to cheer the market as it lacked enough incentives to attract capital flows. However, only a few announcements were made that could be important, for example, the reduction of the withholding tax on long-term infrastructure bonds and allowing FII participation in currency derivatives |

|

|

|

The recent appreciation in the INR has been more tactical than fundamental due to FII bond inflows. However, the large current account deficit and high inflation remains a challenge, which might prevent the RBI from cutting rates sharply |

|

|

|

USD-INR has been trading slightly lower after the budget announcement. However, should there be a better commitment towards improving either the twin deficits or increasing investment flows, the INR would benefit to a more significant degree |

|

|

| Currency Forecast |

|

| |

2012 |

|

|

|

2013 |

|

|

|

| Currency |

Q1 |

Q2 |

Q3 |

Q4f |

Q1f |

Q2f |

Q3f |

Q4f |

| USD/INR |

50.90 |

55.50 |

52.90 |

55.00 |

54.40 |

54.00 |

53.00 |

52.00 |

| EUR/USD |

1.33 |

1.27 |

1.29 |

1.32 |

1.30 |

1.32 |

1.34 |

1.35 |

| GBP/USD |

1.6 |

1.57 |

1.61 |

1.63 |

1.48 |

1.48 |

1.48 |

1.48 |

|

|

|

| Source: HSBC March 2013 Currency Outlook |

| |

| Indicative Rates |

|

| Indian Rupee |

As of Mar. end |

As of Feb. end |

Change |

Asian Indices |

As of

Mar. end |

As of

Feb. end |

Change |

| USD/INR |

54.31 |

54.37 |

-0.11% |

BSE Sensex |

18835.77 |

18861.54 |

-0.14% |

| EUR/INR |

69.57 |

71.03 |

-2.06% |

US Treasuries |

|

|

|

| JPY/INR |

0.5759 |

0.5871 |

-1.91% |

1 year |

0.129 |

0.1529 |

-15.63% |

| GBP/INR |

82.53 |

82.45 |

0.10% |

5 years |

0.7691 |

0.766 |

0.40% |

| CHF/INR |

57.16 |

58.03 |

-1.50% |

10 years |

1.8521 |

1.8808 |

-1.53% |

| AUD/INR |

56.43 |

55.53 |

1.62% |

Commodity |

|

|

|

| Global Indices |

|

|

|

Gold |

1596.17 |

1579 |

1.09% |

| Dow Jones Index |

14578.54 |

14054.49 |

3.73% |

Silver |

28.26 |

28.51 |

-0.88% |

| GOI Bonds |

|

|

|

Crude Oil |

110.02 |

111.38 |

-1.22% |

| 1 year |

7.82 |

7.85 |

-0.38% |

USD/INR Forwards |

|

|

|

| 5 years |

7.96 |

7.92 |

0.51% |

6 months (%) |

7.23% |

7.27% |

-0.59% |

| 10 years |

7.95 |

7.87 |

1.02% |

1 year (%) |

6.70% |

6.61% |

1.33% |

| 6 Months LIBOR |

|

|

|

|

|

|

|

| USD |

0.4449 |

0.4569 |

-2.63% |

|

|

|

|

|

|

|

| Source: Bloomberg/Reuters |

| |

Indian Macro-economic Indicators Released (period 1 March 2013 to

31 March 2013) |

|

| Date |

Time |

Indicator |

Period |

Actual |

Forecast |

Prior |

| 01-Mar-2013 |

10:30 |

India Feb HSBC Markit Manufacturing PMI |

Feb |

54.20 |

- |

53.70 |

| 05-Mar-2013 |

10:30 |

India Feb HSBC Markit Services PMI |

Feb |

54.20 |

- |

57.50 |

| 11-Mar-2013 |

11:00 |

Exports Y-O-Y% |

Feb |

4.2% |

- |

0.8% |

| 11-Mar-2013 |

11:00 |

Imports Y-O-Y% |

Feb |

2.6% |

- |

6.1% |

| 12-Mar-2013 |

11:00 |

Industrial Production Y-O-Y |

Jan |

2.4% |

1.3% |

-0.6% |

| 12-Mar-2013 |

11:00 |

CPI Y-O-Y% |

Feb |

10.91% |

10.60% |

10.79% |

| 14-Mar- 2013 |

11:00 |

WPI Y-O-Y% |

Feb |

6.84% |

6.59% |

6.62% |

| 19 Mar-2013 |

11:00 |

Repo Rate |

- |

7.50% |

7.50% |

7.75% |

|

|

| Source: Bloomberg/Reuters |

|